Common Mistakes in Bookkeeping (Retrospective Tracking)

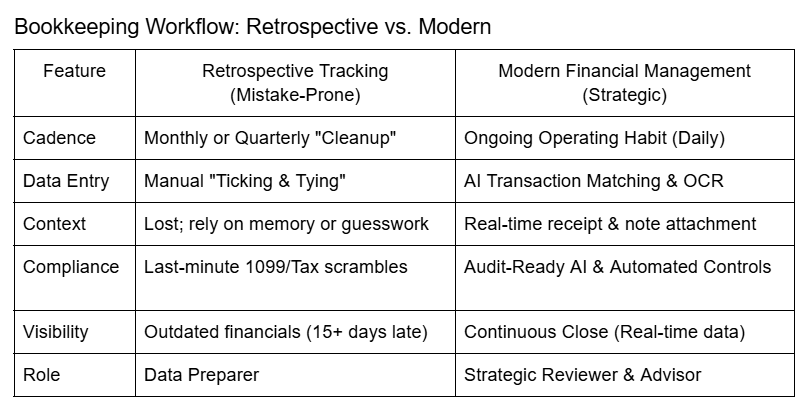

One of the most pervasive mistakes founders make is treating bookkeeping as a retrospective task rather than an ongoing operating habit. When transactions are allowed to pile up until tax season or a moment of cash-flow stress, the critical context behind each expense is often lost. This led to a reliance on guesswork, where bookkeepers must categorize transactions based solely on vendor names, often resulting in messy books filled with "miscellaneous" or "uncategorized" entries. Furthermore, delaying these core tasks frequently results in missing receipts and a month-end close that stretches beyond the 15-day mark, rendering the resulting financial reports outdated and useless for real-time decision-making.

Retrospective tracking also leads to significant compliance and tax-related oversights that can compound silently. For instance, many businesses fail to collect W-9 forms from contractors before the first payment is issued, leading to a frantic scramble in January and potential IRS penalties. Additionally, firms that wait to review their records often overlook sales and use tax obligations, specifically failing to identify a "nexus" in new states as they grow. Another common pitfall is staying on a cash basis of accounting for too long; while simple, this method can distort the performance of businesses with subscriptions or annual contracts, whereas accrual accounting provides a much clearer picture of long-term financial health.

Utilizing outside and online bookkeeping services provides a strategic solution to these manual errors by implementing an integrated tech stack that automates the "ticking and tying" of ledgers. These virtual services leverage cloud-based tools to enable automatic receipt matching and bank feed integrations, ensuring that data is captured at the point of purchase. Furthermore, outside firms offer scalability, allowing a business to pay only for the level of support they currently require while gaining access to a specialized depth of accounting knowledge regarding 2026 tax code sunsets and new pay transparency laws. By moving the books to a secure, SOC II certified online environment, founders also benefit from enhanced data security that far exceeds typical in-house capabilities.

Ultimately, the digital transformation of financial management is shifting the professional's role from a manual preparer to a strategic reviewer. Through a "continuous close" model, where AI agents reconcile and monitor data in real-time, the traditional month-end "fire drill" is replaced by a constant, proactive flow of information. This allows the bookkeeper to act as a trusted advisor, using clean data to perform scenario analysis and engage in financial storytelling. By embedding these tasks into daily workflows, businesses maintain audit-ready AI systems that satisfy board-level scrutiny and provide a single source of truth for growth.

Key Words & Concepts

Continuous Close: A real-time accounting process where reconciliation and anomaly detection run in the background daily.

Ongoing Operating Habit: The mindset of recording transactions and attaching documentation as they occur to prevent the loss of context.

Integrated Tech Stack: A harmonious ecosystem of cloud-based applications that talk to each other to reduce manual work and data silos.

Strategic Reviewer: The modern professional who oversees automated system outputs and provides high-level judgment and guidance.

Audit-Ready AI: Systems engineered to be auditable and explainable to satisfy regulatory and board-level scrutiny.